Verticals in the Age of AI

Trying to piece together the transformation of knowledge work.

I recently read a tweet by Josh Hunt postulating that the UK as a service economy is significantly more exposed to AI than other countries:

81% of UK GDP is services. 83% of UK employment is services. Law. Finance. Consulting. Admin. Media. Tech. Middle management. These aren't side categories. They are the British economy.

They are also the roles with the highest AI exposure.

Goldman Sachs ranks them at the top: legal, financial analysis, operations, content production. The IMF puts 70% of UK workers in AI-exposed occupations, against around 60% in the US.

It got me thinking, what will all these people do?

Currently they exist in some knowledge work vertical: design studio, recruitment firm, video production, investment banking, etc.

They can't simply “move to AI”. As I've said before, you can't pivot into AI. AI is so ubiquitous that every industry is already transforming.

A yoga studio still needs human yoga instructors. But its marketing, branding, scheduling, student relationship management, and digital products will all be changed.

But it's fair to say that yoga studios will be more resilient compared to tech companies. No risk, no reward, investing in tech means you may be focusing on obsolete workflows but there's bigger rewards if you figure out where the puck will go.

Specifically for knowledge work, however, I do think there is a universal pattern emerging. Every industry is being restructured according to this pattern.

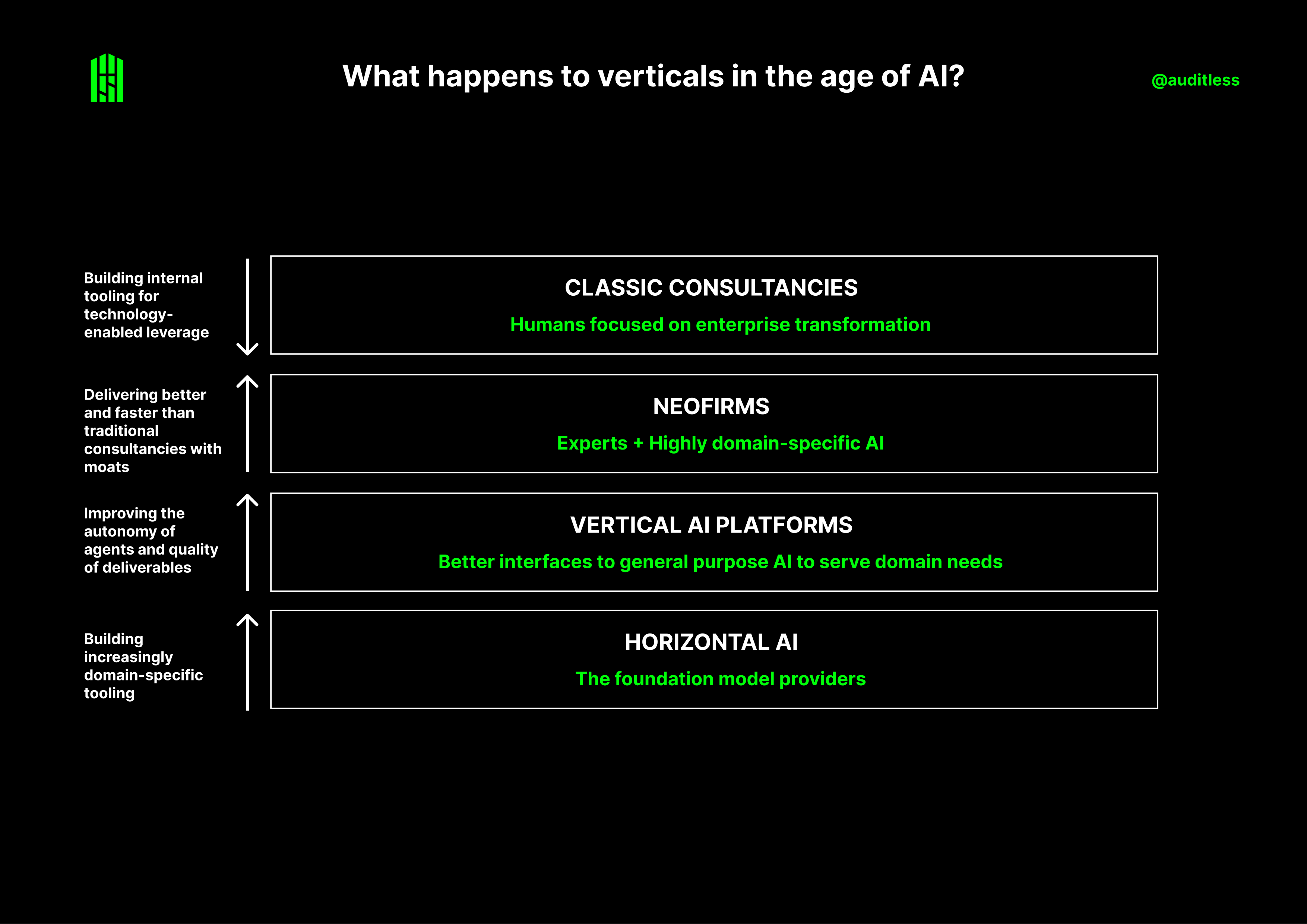

There are 4 layers in each vertical that will matter:

Horizontal AI (model providers)

Vertical AI (domain-specific wrapper interfaces)

Neofirms (AI-powered consultancies)

Classic Consultancies (transformation firms)

Horizontal AI is the EVER-EXPANDING BLOB

“Why wouldn’t OpenAI or Anthropic just build this?”

Every Founder now has to answer this question.

Previously, whether you built a marketplace or a social network, there was always the question of why Google or Facebook wouldn’t copy it. But it was much easier to find compelling answers back then. Those companies had to make a conscious effort to enter a market. Now, models are inherently general. Their range expends as a function of general intelligence.

At an extreme, if models reach AGI, the final barrier will be compute cost. We’re not there yet. But horizontal AI providers are already a dominant participant in every vertical. And this category isn’t just OpenAI and Anthropic. It includes open source models and future market entrants.

Vertical AI platforms compete on INTERFACE and INTEGRATIONS

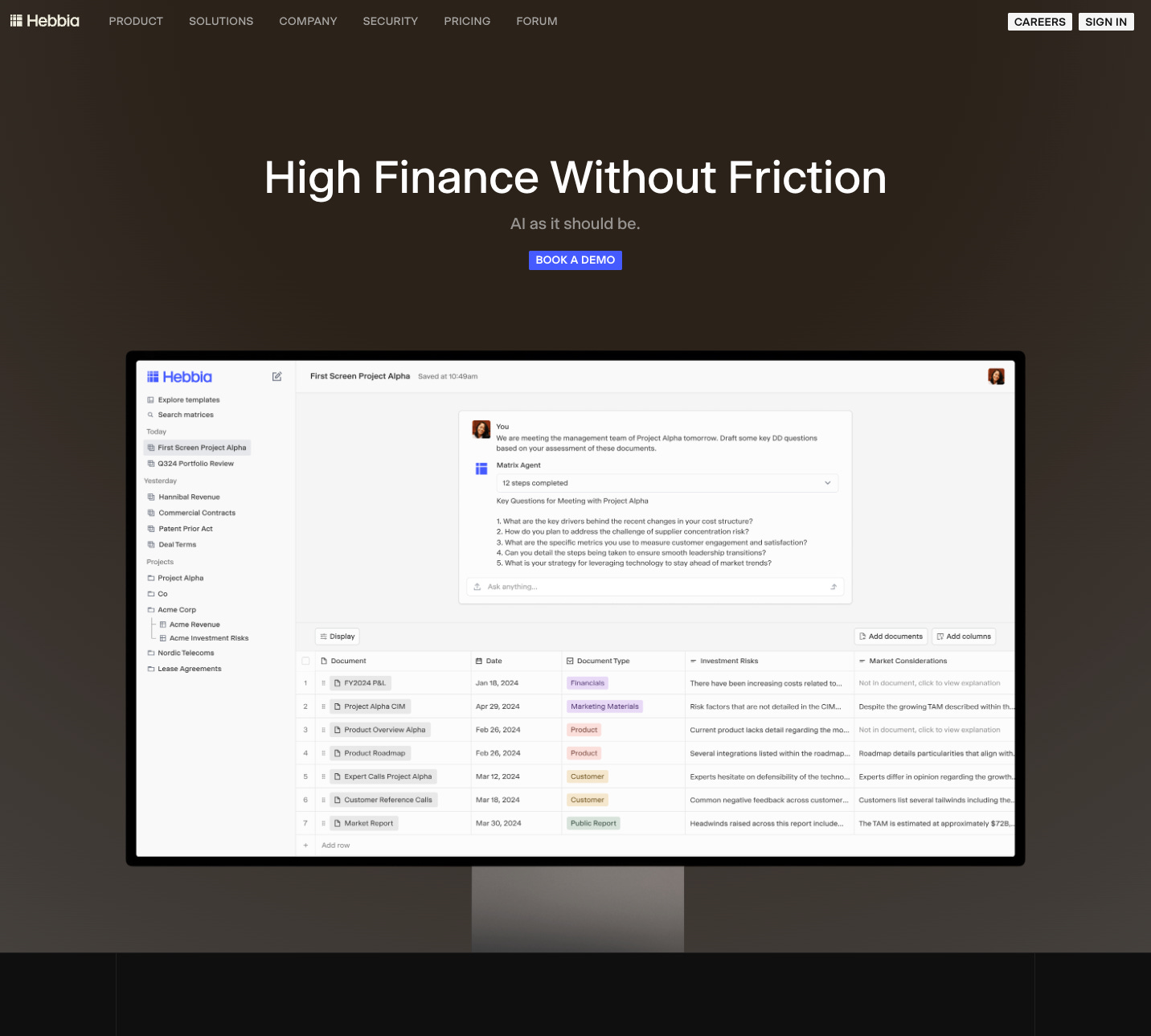

Vertical AI platforms are copilot software that works alongside knowledge workers for domain-specific tasks. Engineers use Lovable, lawyers use Harvey and bankers use Hebbia.

They largely rely on the same underlying models but deliver higher value through better interfaces and better agentic workflows. Hebbia‘s Matrix product is a good example.

The platform changes the default output from an AI model from text to a table. Rows are different sources, columns are different questions you ask of those sources. It’s essentially a pivot table for extracting knowledge from AI.

Behind the scenes there’s an improved data extraction pipeline that emulates a bigger context window but a lot of the value is just this interface that’s better suited to how financial professionals actually work. Synthesising information from disparate sources, being rigorous about referencing and ingesting private reports.

The tension is that horizontal platforms are dipping into domain-specific workflows. Anthropic is building tools for Claude to work inside presentations and spreadsheets. OpenAI ships Codex. Both are partnering with enterprises and creating vertical-specific benchmarks. Meanwhile, vertical AI platforms are pushing the other direction: improving the quality and autonomy of their agents, working to make deliverables more viable as finished output. The battleground between these two layers is active and accelerating.

Neofirms are the POWER USERS of AI

Neofirms are consultancies that are highly AI-leveraged.

They combine people with proprietary AI tooling (where the AI does a significant portion of the work) and people review it or collaborate with it. They can deliver better and faster than traditional consultancies.

Crosby coined the term “neofirm” in law. They’re a registered law firm that uses AI agents and in-house lawyers together to review, redline, and negotiate contracts rapidly and at a fraction of the cost of traditional firms.

What makes neofirms interesting as a category is that they sidestep the biggest obstacle vertical AI platforms face which is education.

If you’re building a vertical AI platform, you can have brilliant ideas about how professionals should be using AI in law or finance. But those ideas are only as good as the customers implementing them. A neofirm doesn’t need to educate customers. It can run ahead to the future and use the most advanced AI workflows, focusing entirely on delivering outcomes.

Neofirms also get to be more opinionated about proprietary data they absorb and work on while vertical AI platforms are investing in replicating similar interfaces to horizontal AI companies.

Classic consultancies own the transformation

Classic consultancies are existing large firms focused on holistic transformation. Transformation is not a technology problem. These firms work with leadership and management to implement projects and incorporate partnerships across all three previous layers.

Their revenue base demands bigger partnerships with large companies and that will continue to be the bread and butter. They’ll build internal tooling for technology-enabled leverage and compete with neofirms at the edges. Neofirms in turn, will try to deliver better and faster, push the price point down, and do so with more compounding technology and data moats. Classic consultancies risk relying too much on internal expert networks at the expense of the kind of systematic data advantage that neofirms are building. But their grip on enterprise relationships and change management is durable.

It’s likely that classic consultancies will start acquiring and incorporating neofirms into their delivery model. The two categories need each other more than either would probably admit.

Layers will collide

The interplay between these four layers explains a lot of the dynamics we’re seeing across knowledge work verticals right now.

+ Horizontal AI is not swallowing everything. There’s still a large surface area of different types of work remaining across the other three layers.

+ Neofirms will have an identity crisis. Are they VC-scale technology companies or are they boutique services firms?

+ Services are showing up in unexpected places. Because three of these four layers are effectively productized services, you’ll see companies that traditionally don’t think of themselves as service businesses adding service aspects.

Two-sided marketplaces can offer services on both sides of the market. Jack & Jill is an example: if you’re looking for a job, they give you an AI agent that does coaching and matching. If you’re looking to hire, you talk to an agent that finds candidates and makes introductions. The value floor is a productized service on each side. The ceiling is marketplace dynamics where they accumulate demand and supply and start matching over time.

Using productized service to bootstrap a marketplace is a pattern we’ll see a lot more of.

If you’re part of the service economy, think about where you want to end up. If you want to focus on transformation, classic consultancies are fine. If you enjoy working directly with AI to produce deliverables, a neofirm is probably a better fit. If you’re drawn to the technology itself, maybe you want to build vertical AI.

A little awareness for the end game will help a lot.