UniswapX is a Power Play

How Uniswap had to hurt Liquidity Providers in the short-term to thrive.

Thanks for the support ❤️

Very thankful for some positive messages about the newsletter recently. I learned that it can be a great idea to forward the newsletter to your whole team AND that one of the smartest people in the whole space is an OG reader.

UniswapX may not be the loudest of Uniswap's 2023 launches, often lauded as simply a clone of CowSwap.

But it's their most important strategic play.

It's the first time they didn't prioritize their Liquidity Providers (at least in the short term), instead going for market power.

UniswapX in a nutshell

In essence, UniswapX is a way of creating market orders through signing a transaction (but not executing one).

Users sign market orders (or intents to swap).

Participants called “Fillers” compete to execute orders most fairly.

Competition happens through a Dutch Auction. The order starts at a non-competitive price and the price continuously decreases according to a decay formula until it is filled at the most competitive price.

Fillers can use whatever liquidity is available whether through AMMs (both Uniswap and others), off-chain exchanges or other DEX aggregators to satisfy the order.

The protocol prevents Fillers from extracting too much value from the Swapper by incentivizing them to fill the order as soon as incrementally profitable.

UniswapX through the lens of Aggregation Theory

To understand it, we have to refer to Aggregation Theory, a strategy coined by Ben Thompson underpinning the success of the world’s largest tech companies like Apple, Meta, Google, Microsoft.

(Note: these aggregators are different from DEX aggregators.)

UniswapX fits Ben Thompson's definition in Defining Aggregators perfectly.

He defined an Aggregator as a company with the following 3 characteristics:

Direct Relationship with User ✅ (the users are Swappers in this case)

Zero Marginal Costs For Serving Users ✅ (we’re in crypto after all)

Demand-driven Multi-sided Networks with Decreasing Acquisition Costs ✅ (the network is multi-sided through participation of Swappers and Fillers with clear incentives for Fillers to participate)

But the reason this move is so surprising is that Uniswap's customer has not been the Swapper.

Uniswap’s core customer persona has always been the Liquidity Provider.

Let's recap.

Going beyond the Liquidity Provider

AMMs are ultimately a vehicle enabling passive liquidity provision.

When Uniswap launched routing, it only routed to its own Liquidity Providers.

With V3, Uniswap allowed LPs to earn more fees.

With V4, Uniswap allowed Liquidity Providers to leverage Hooks.

Even the Uniswap wallet, while designed to help users, prioritizes Uniswap as the default AMM.

With UniswapX, orders will now be routed to other venues to help Swappers get the best possible execution.

So orders may get routed away from Uniswap’s Liquidity Providers at least in the short term.

Dan Robinson hinted this in his tweet:

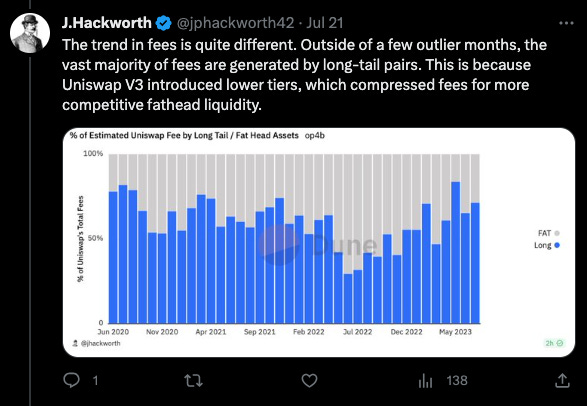

J. Hackworth’s analysis is interesting to look at, he explains why Uniswap's stronghold of long-tail assets won't get displaced.

In the long term, this could attract more swappers to trade through the Uniswap front-end and restore volume to Liquidity Providers.

Time will tell what this means for LP profitability in the Uniswap protocol, but there are clear benefits for Uniswap overall:

It ensures fair play by making sure Uniswap cannot be disaggregated easily. This is potentially a risk mitigating move. To the extent that users are becoming more aware of the risks of MEV, they were at risk of moving to other RFQ or auction based platforms already

It eats into fee revenues of other DEX aggregators (1Inch) and meta DEX aggregators (CowSwap) by forcing them to compete with other aggregators and with UniswapX

Uniswap is creating a new revenue stream from UniswapX Swapper fees.

So how can you start thinking about your Aggregation Theory play?

Step 1. Identify the Platforms that disintermediate your users

Think about who is fulfilling user intents in your ecosystem.

When AMMs were new, Uniswap had fairly direct access to swappers.

Eventually aggregators like 1inch emerged, so Uniswap built their own router.

But then meta-aggregators like CowSwap emerged and many more intent-based systems were detailed.

It was clear Uniswap was at a risk of being disintermediated.

Step 2. Be prepared to cannibalize yourself

The winning aggregator is one that serves the dedicated end-user best.

Uniswap's position is analogous to Google. While Google’s user is the search user, their customer is really the Advertiser (liquidity provider in Uniswap’s case).

The threat of LLMs is very challenging for Google. On one hand, to provide the best search experience, they have to aggressively integrate LLMs.

On the other hand this may make ad-based answers less prominent and hurt Google’s ad revenue.

Ultimately, if LLMs have a threat of becoming the entry point for search, Google has to be willing to cannibalize or evolve their advertising offering to not lose the aggregator position.

Step 3. Make something 10x better for the target user

Aggregators are sticky.

Many users stick with the same bank, search engine, wallet, dex aggregator.

To disrupt that and become the leading aggregator for end-users, you have to innovate and create something better than existing aggregators.

UniswapX does have some distinctive features. The optional RFQ mode is interesting and cross-chain swapping is possibly the first instance of a working cross-chain intents based system.

Step 4. Leverage your existing assets

Uniswap can now leverage their existing surfaces like the mobile wallet and web interface and they should.

Previously these surfaces may have been created “for the benefit of LPs” by prioritizing Uniswap swaps and not featuring other venues.

Now, it’s clear that both these surfaces are liable to serve Uniswap as a whole more than Uniswap's LPs.

It’s a tradeoff they had to make.

To learn more about Aggregation Theory, you’ll want to look up Ben Thompson's resources on the topic.